The topics of the table of contents can be selected directly via the blue links. With the additional scroll bar on the right side, the description can be quickly traversed over large areas. In addition to the algebraic and trigonometric basic operations, the calculator allows the following calculations via special function buttons: Conversion of interest rates taking into account compound interests for the following time units, year, quarter of a year, month, week or day and vice versa, calculation of the effective interest rates for various interest time periods during the year, instalment savings with and without start deposit, determination of payment by instalments depending on different running times and interest rates, calculation of rest book values for annual linear, digressive or progressive depreciation. Calculation of leasing payments with and without down payment, different running times and effective interest rates to determine the rest book value, the leasing rates per month and the pure monthly costs of leasing.

Terms of use and first steps.

The calculator is a development of the homepage author. It is only allowed to use the PHP calculator freely via the private homepage "https://ARTandENGINEERING.net". It is not permitted to copy the calculator or use and distribute it commercially. The various applications of the calculator are explained in detail in the manual by means of examples. The free use of the calculated results are made under your own responsibility, legal claims from the user to the author are excluded.

Decimal numbers are written in the United Kingdom with a dot and on the continent in Europe with a comma. In order to apply the calculator widely, both the dot and the comma are used in a number as one and the same decimal character. Large numbers are often divided into three-digit ranges, in the UK with a comma and on the continent in Europe with a dot. This notation is not allowed and is misinterpreted by the calculator.

With the buttons [X-field], [Y-field] and [Z-field] the input fields X, Y and Z can be selected directly. The internal keyboard of a mobile phone or of a touch screen computer does not jump over the surface of the PHP Calculator. In case there is no touch screen monitor available, as on a normal PC, the input fields can also be addressed with a mouse click.

Depending on the task, up to 5 numerical values are entered in the 3 input fields X, Y and Z. Two values are separated e.g. with a logical & (123 & 456). If you jump back after an operation with the Back Space key, the input data are displayed again in the input fields. They can be altered easily (for further information see here 09 Input Fields and Input Data.).

The internal operations of the calculator are programmed in the dynamic, server-oriented language PHP and run on an external PHP server. The calculator is password protected. The calculator is unlocked for 20 minutes. Then follows the note: "The usage time has expired !". For the re-activation, the blue links 'Unlock the calculator here.' in the headline of the PHP Calculator and in the table of contents of the homepage the chapter 3.2 are to click.

In addition to the homepage calculator are more functionally identical mobile phone calculators in German available which automatically adjust themselves to the display size of a mobile phone. While the adjoining calculator exists only once, several mobile phone calculators can be used parallel in time sharing. The activation of the mobile phone calculators can be done with the adjoining calculator, even in case it should be occupied. In the X-field MWD is entered, then the button [enter] is pressed and finally the link "Load Smart Phone Version?" has to be activated in the result field. The usage time of the mobile phone calculator is limited to 30 minutes. The predetermined time limit is used for the automatic release of the calculators when they are no longer used. But after each expiry of the time limit, another mobile phone calculator can be activated. There is no connection between the individual mobile phone calculators; a busy calculator cannot be occupied via its link to the server. The non-limited use is only possible after an agreement with the author (request via email address, see Imprint).

Button: Alter Time Unit Convert interest rate / year to the month or the week or the day and vice versa. The exponential compound interest calculation is used.

X-field: Enter the interest rate per previous unit of time. Y-field: Enter the abbreviation (see table) for the conversion to the interest rate per desired unit of time.

Example 1: An interest rate / year of 7% has to be converted to an interest rate / month. Entries: X field: 7 and Y-field: J, M. Then press the button [Alter Time Unit]. Result: interest rate / month = 0.5654%. The conversion was made on the condition that the interest rate is cedited only once after each year, i.e. compound interest comes only into force after one year. Would a banking business be ended after 3 months, one could calculate with the interest rate per month the accrued interest.

Further conversions according to the following table:

Input field X:

Input field Y:

Result:

interest rate / year

J,3M

interest rate / quarter

interest rate / year

J,M

interest rate / month

interest rate / year

J,W

interest rate / week

interest rate / year

J,D

interest rate / day

interest rate / quarter

3M,J

interest rate / year

interest rate / month

M,J

interest rate / year

interest rate / week

W,J

interest rate / year

interest rate / day

D,J

interest rate / year

nominal interest rate/year

J,MJ

effective interest rate/year

effective interest rate/year

MJ,J

nominal interest rate/year

If the interest payment is made several times within a year, this is called interest during the year. The interest credit leads already in the current year to a compound interest. The annual interest rate increases to an effective interest rate per annum. The number of interest periods within one year have to be entered in the Z-field. The following interest periods are possible: Half-yearly z = 2, quarterly z = 4, monthly z = 12, weekly z = 52, daily z = 360 and continuously z = && (continuous interest). The &&-sign introduces a limit analysis for the interest rate calculation. There are an infinite number of interest periods over the year.

Example 2: The nominal interest rate per year is 6%. The interest is credited quarterly. Entries: X-field: 6, Y-field: J,MJ und Z-field: 4.

Then press the button [Alter Time Unit]. Result: effective interest rate / year = 6.136355%. The interest rate was converted to a full year interest period.

It is advisable to use at least 4 digits behind the comma in case of interest rates per month and 6 digits in case of interest rates per day, as the rounding errors increase. Comparative results, exactly to one cent, are only obtained with 6 digits behind the comma !

In the exponential compound interest calculation, there is no linear relationship between the monthly, weekly or daily interest rate, i.e. an annual interest rate cannot simply be divided by 12 to get the monthly interest rate.

Button: End Capital

End Capital = Interest on the starting capital over a defined period of time. The exponential compound interest calculation is used.

Example: interest rate / year x = 10%, starting capital y = € 100, running time z = 2 years. Entries:

X-field: 10, Y-field: 100 und Z-field: 2.

Result: E = € 121 under a one-year interest rate period.

An interest rate of 10% per annum leads to the same interest income as the interest rates of 0.7974% per month or 0.183457% per week or 0.026479% per day. The conversion of the interest rates is done with the button [Alter Time Unit]. Interest rate and period of time are always based on the same unit of time (see below table):

Interest Rate

Starting Capital

Period of Time

End Capital

per year x = 10 %

y = € 100

z = 2 years

E = € 121

per month x = 0,7974 %

y = € 100

z = 24 months

E = € 121

per week x = 0,183457 %

y = € 100

z = 104 weeks

E = € 121

per day x = 0,026479 %

y = € 100

z = 720 days

E = € 121

The interest rates relating to the month, the week and the day have each been converted to a different time unit of the annual interest period.

An annual nominal interest rate of Pnom = 6% increases in case of a quarterly interest rate to Peff = 6.136355 % per year (see example 2 above). If the the total term would be 2 years, 8 months and 5 days, the time would be in years: z = (2x360 + 8x30 + 5)/360 = 2.68055555 years. The inputs for the effective interest on a starting capital of € 1000, - are: X-field: 6.136355, Y-field: 1000 und Z-field: 2.6805555.

Then press the button [End Capital].

Result: € 1173.09 under a quarterly interest credit. With an annual interest credit, it would only be € 1169.05.

Computationally, the conversion of the effective interest rate per year from 6.136355% to an effective interest rate per day leads to the same final capital of € 1173.09 if the run-time of 965 days is entered in the Z-field instead of 2.6805555 years.

In addition to the exponential interest rate, financial mathematics offers a linear, mixed and continuous interest rate. Interest periods usually coincide with the turn of the year. In the case of mixed interest rates, exponential interest rates are charged for the full interest periods, whereas a linear interest rate is provided for the possible incomplete interest periods at the beginning and at the end of the whole term. With continuous interest rates, the number of interest-rate periods within a year is infinitely large; it is a continuous interest. Depending on the valuation practice of the bank, the first day but not the last day or the last day and not the first day are included in the interest calculation. It would be necessary to clarify with the bank which interest period the investments or loans are subject to. An annual interest period would be better for the borrower and worse for the investor. In the credit service sector and financial world, the term effective interest rate or annual percentage rate (APR) has a complementary meaning. It also includes certain fees and processing costs that would need to be scrutinised.

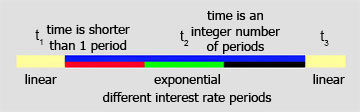

Button: End Capital with mixed Interest Rates.

The total time of the interest is t = t1+ t2 + t3. The times t1 and t3 are part times of a full period of time counted in days. For t1 and t3 a linear interest rate per day is applied. The main time t2 consists of one or several defined periods of time which coincide with the turn of the year. For the main time t2 an exponential interest is applied. The individual periods for t2 can be: one year, a quarter of a year, one month or one week, etc. For shorter periods then one year, an effective interest rate related to the year or the month will be calculated first. This calculated effective interest rate is then linearly broken down to a linear effective rate per day for the terms t1 and t3.

The entries for the calculator are: X-field: Effective interest rate per year resp. per month. Y-field: Starting Capital. Z-field: D days of the fractional period of time t1 at the beginning , M months resp. J years of the main time t2, D days of the fractional period of time t3 at the end. Before entering the numerical values, the time characterising letters D, M resp. J are entered in the Z-field with or without emty digits.

Example: 5 % nominal interest rate per year and a quarterly interest period of time. Starting Capital € 5000,-, total term of time 6 years, 7 month and 5 days. Start of the first full period of time after 70 days. Results: Effective interest rate per year = 5.094534 % resp. per month = 0.414942 %.

Total term of time for t2 + t3 = 360x6 + 30x7 + 5 - 70 = 2305 days. 2305/90 = 25 quarters + 55 Tage.

( t1 = 70 days, t2 = 75 months bzw. 6.25 years, t3 = 55 days). Entries for an effective interest rate per month: X-field: 0.414942, Y-field: 5000 und Z-field: D 70 M 75 D 55. End Capital: € 6942.15.

Entries for an effective interest rate per year: X-field: 5.094534, Y-field: 5000 und Z-field: D 70 J 6.25 D 55.

End Capital: € 6942.15.

The following calculation models for instalment savings, payment by instalments and leasing are based on the exponential interest rate with an effective interest rate per month over the entire term. The effective interest rate can be set for the whole year or calculated for shorter periods of time during the year depending on the specification.

Button: Saving Sum, monthly instalment savings without start deposit.

The total savings amount E is calculated with a uniform monthly savings deposit (rate / month) y and with a monthly interest rate of x% over a period of z months.

Example: interest rate / month x = 0.56%, rate / month

y = € 100, periods of time z = 60 month (5 years), insert in the X-field: 0.56, Y-field: 100 and Z-field: 60. Result: ∑ Savings E = € 7147.45.

Monthly instalment savings with start deposit.

Example: interest rate / month x = 0.45%, Start deposit yo = € 960. In the following months a monthly rate of

y = € 80 will be paid in for z = 60 month.

Entries X-field: 0.45, Y-field: 960 & 80, Z-field: 60. Result: ∑ Savings E = € 6783.57 at the end of the 61st month after the beginning.

In the Y-field between the start deposit yo

and the monthly rate y the &-sign is set.

Button: Monthly Rate,

payment by instalments, pay back a credit.

Calculates the monthly repayment rate R for a loan amount y, with a monthly interest rate of x% over the entire term of z months.

Example: interest rate / month x = 0.5%, loan amount

y = € 10 000, period of time z = 24 month, insert in the X-field: 0.5, Y-field: 10 000 and Z-field: 24. Result: repayment rate R = € 443.21 per month, repayment sum in 24 month ∑ R = € 10 636.95. Conclusion: The loan costs in 2 years without the fees of processing 636.95.

Button: Rest Book Value, linear, digressive or progressive depreciation.

Calculation of the annual depreciation amount and the rest book value.

Inputs:

X-field: usage year x (depreciation year);

Y-field: initial value y (start value);

Z-field: useful life time z of the object in years.

Outputs: R: Rest Book Value; A: Write off Value (depreciation amount);

J: Write off Year.

The depreciation type (linear, digressive or progressive) can be selected with the respective radio button. The proper depreciation method is defined in the respective countries by the tax and commercial law. The depreciation period can be found in so-called depreciation tables.

Example: An investment of € 21 000 should be written off in 7 years. What is the rest book value R and the depreciation amount A at the end of the fifth year J in a linear depreciation? Result: R: € 6 000; A: € 3 000; J: 5.

With a leasing contract, the rights of use of an object are acquired. The owner is and remains the lessor. The total amount of the lease is composed of the acquisition of the property, the administrative costs, the capital financing, possible bonuses payments and ultimately also the lessor's compounded return. With the exception of additional services, service leasing, in the case of a car, the lessee is the keeper of the car responsible for the insurance and maintenance of the car. The annual mileage, the term of the lease, the total amount of the leasing and the amount of the down payment determine the monthly leasing rate over the effective leasing interest rate. Depreciation is done according to the tax law or corresponding depreciation tables; e.g. for cars linear over 6 years. It has to be distinguished between a tax depreciation period, which is fixed in the case of a car, and the computational depreciation time in a leasing model. In the lease model, the total depreciation time may include one or more lease terms with one or more lessees. The individual lease terms may e.g. vary from 2 to 6 years and include very different mileage, which in turn may be between 15 000 and 180 000 km according to the needs of the lessee. The monthly leasing rate is therefore crucially determined by the annual mileage. The vehicle is either sold after its leasing period at the rest book value or re-leased. From a purely computational point of view, the entire depreciation period can be extended with a low annual mileage. By specifying the annual mileage, the leasing rate and the leasing costs per month and per kilometre can be determined. This gives you transparent parameters for comparing different leasing providers.

For the calculation model used, the effective interest rate applied by the lessor is used in accordance with the rules of the banking industry. In other words, the leasing rate is to be used as the loan repayment rate for the consumed value components, including compound interest, the outstanding depreciation and the rest book value.

Leasing contracts offer a wide play field in terms of time, leasing interest rate, leasing rate and rest book value. Low leasing rates increase the rest book value, possibly creating a gap between the replacement value of the vehicle after a total loss, which should be covered by a comprehensive insurance, and the remaining outstanding lease book value. The lessee is therefore well advised to hedge against this funding gap by means of an additional insurance, the GAP insurance. It must also be ensured that the lessee is not obliged to take over the vehicle at the rest book value after the leasing term has expired. In the following 5 examples only net values of the leasing are considered and not the additional insurance amounts and the VAT.

Inputs: X-field: effective leasing interest rate per month. Y-field: total assets & down payment of the leasing object. Z-Feld: total depreciation tme in month & leasing time in month. (Alternative Input for the Z-field see Leasing Example 4.) Outputs: Residual book value, the leasing rate per month and the leasing costs per month.

The leasing costs due to the interest are included in the leasing rate. (If the effective leasing rate were 0%, there would be no leasing costs. The lease rate would then include only the consumed value share. The calculator also allows the entry of a negative, fictitious leasing interest rate, which would lead to negative leasing costs. Negative leasing costs would add up to a reduction of the total assets over the lease term.).

Example 1 (car leasing): Effective leasing interest rate per year are 5%, total leasing value € 49 000.-, down payment € 15 000.-, total depreciation time 6 years, leasing term 3 years.

First, the leasing interest rate is to be converted to the month:

Inputs: X-field: 5; Y-field: J,M; Then press the button [Alter Time Unit]. Interim result: interest rate per month x = 0.4074 %. For the further calculation, the radio button X (R) has to be activated, the interest rate per month x = 0.4074% is automatically assigned to the X-field. (It is advantageous for additional calculations to save the value also to a store with the button [store]. With the radio button X (S), the leasing interest rate per month could then be reassigned to the X field several times). Further inputs to Example 1: Y-field: 49 000&15 000 and Z-field: 72 & 36 (The time values are to be entered in months). Activate the radio button "lease" and press the button [Rest Book Value]. Results 1: Rest Book Value € 17 000.-;

Leasing Rate / M € 583.09; Leasing Costs / M € 110.87.

Example 2: If according to Example 1 the down payment were cancelled under otherwise identical conditions, the Results 2 would be:

Rest Book Value € 24 500.-; Leasing Rate / M € 840.33;

Leasing Costs / M € 159.78.

Example 3:

If, assuming a down payment of € 15 000, - and a leasing time of 36 months, according to Example 1 the effective leasing interest rate were instead of 5% p.a. only 2.5% p.a. the Results 3 would be:

Rest Book Value € 17 000.-; Leasing Rate / M € 526.75;

Leasing Costs / M: € 54.53.

The mileage in the above examples should be between 20 000 and 30 000 km per year over the six-year depreciation period. With the given mileage, the leasing rate and the leasing costs per month and per kilometre can be determined. This gives the lessee transparent comparative variables of different providers. Example 2, without a down payment, would be advantageous for a commercial user since he can immediately write off the monthly leasing instalment. The leased object is cost-neutral for him from the procurement point of view.

Example 4: Example 3 may not be attractive enough for the private lessee. With the limitation of the annual mileage to 10000 km, the lessor could, for example, extend the depreciation period from 6 to 11 years. This would lead to the following data: Result 4: Resst Book Value: € 24 727.27; Leasing Rate / M: € 320.33; Leasing Costs / M: € 62.75.

The same result would be obtained in case the lessor set the rest book value to € 24 727.27 without mentioning the total depreciation time. The inputs would lead to the following data:: X-field: 0.206 Y-field: 49 000&15 000 Z-field: 24 727.27 M 36. Note the placeholder M instead of &. Further explanations will be found in Example 5. If the 10 000 km are exceeded in a narrow range, additional costs per kilometre are incurred (for example € 0.29 / km). In the case of falling in a small limit below 10 000 km, costs per kilometre may be credited (for example, € 0.09 / km). With the specification of the kilometre mileage, the leasing rate per month and per kilometre can always be determined.

Example 5:

Universal Application. Lessee specifies the desired leasing time (4 years or 48 month) and the maximum down payment (€ 2 000.-). Lessor offers only the purchase value of the vehicle (€ 39 455.-) and the leasing rate per month (€ 674.66).

Unknown are the effective interest rate per month and the rest book value. The lessor is not willing to let you know the data for business reasons. But the two unknown data can be determined with the calculator.

Since cars are normally totally depreciated after 6 years (72 month), the lessee can calculate iterative the effective interest rate per month, the leasing costs per month and the rest book value. Starting with 0% in the X-field, you change the interest rate per month in small steps until the leasing rate per month matches with the mentioned one (€ 674.66) of the lessor. The interest rate per month can then be used to decide whether it is better to obtain a loan through the bank or take an offer from another lessor.

Results: effective Interest Rate / M 0.56 %; Leasing Costs / M € 154.45; Rest Book Value € 12 485.

The given examples with the fictitious numbers refer only to net values, i.e. without VAT and insurance costs and should only show the possibilities with the PHP Calculator. You get transparent sizes for the comparison of different providers. Before signing a leasing contract, you should first inform yourself thoroughly about potential pitfalls.

Values are entered only in the X-field. Examples: sin(x) value of x = 30 degrees. Result 0.5 arc sin is the inverse function of the sin function. Example: arc sin(x) value of x = 0.5. Result 30 degrees.

Button: x exp y means the value of x is raised to the power of y ( xy ). Example: 24, Input X-field: 2 and Y-field: 4. Result 16. With this function also root operations can be performed. The nth root of x is equivalent to x(1/n). The value 1 / n is calculated first, if necessary, stored with the button [store]. Example: 4th root of the value x = 16 with y = 1/4 = 0.25 (use only the decimal number in the Y-field). Result: 2. Example: 2.5th root of the value x = 16 with y = 1/2.5 = 0.4. Result: 3.0314331330208.

e exp y means the Euler number e is raised to the power of y ( ey ). e = x = 2.7182818284591. ey can be calculated in the form

xy = 2.7182818284591y.

Button: 10^ means input an integer exponent to the base 10. In the X-, Y- or Z-field the letter E is written. Example: 1.25E-5 = 0,0000125. 1E-5 is identical to 10-5. In the input fields very small or very large numbers can be processed. There is always a number before the letter E. In the simplest case, it is 1, e.g. 107 = 1E+7.

The + sign can be omitted. The expression 3.25E25.46 can not be processed in one step because the exponent is an odd number. 2 operations are necessary. 3.25x1025,46 = 9.3731023851615x1025 = 9.3731023851615E+25.

Explanation of the solution: 1. Operation: Write in the X-field 10 or 1E1 and the Y-field 25.46. Then press the button [x exp y].

The result is saved with the button [store]. 2. Operation: Write in the X-field 3.25, then activate the radio-buttonY(S). The stored value of the first operation is assigned to the Y-field. Finally, press the button [x · y].

Button: ln (x) means the natural logarithm x. Examplel: ln(e) = ln(2.7182818284591), Result 1.

Button: log(x) means the logarithm x to the base 10.

Example: log(10), Result 1.

Not all functions require several Input data in the Input fields X, Y and Z at the same time. Pressing a function key empties the Input fields; only the result is displayed in the Output field 'Result'. If you jump back with the Back Space key, the input values are visible again and can be corrected in the X-, Y- and Z-field. The last contents of the working memory (RAM) and the store (ROM) do not change due to the jump back with the Back Space key. With the radio button underneath the name 'Result' of the Output field the allocation of memory data in the Input fields X and Y are deactivated. The input value of the store doesn't get lost even if the calculator is restarted.

In the Input fields X, Y and Z up to 20 digits can be entered; at least 15 digits are visible. In case of larger numbers, the first numbers disappear behind the boundaries of the Input field but they dont get lost. The calculator can output numbers in exponential notation with 300 and more zeros in the form 1.0 E + 300 = 10+300 resp. 1.0 E - 300 = 10-300 . After a mathematical operation 20 digits can be represented, 15 for the decimal number, including the decimal dot or the decimal comma, and 5 for the representation of the exponent.

The entries in the fields X, Y and Z are deleted by pressing the keys [delsto] or [delram].

The data from the working memory (RAM) and from the store (ROM) can be assigned directly to the X-field and / or Y-field. To do this, the radio buttons are activated.

Example: When the radio buttonX(R) is activated, the last value of the working memory (RAM) or the last visible value from the result field is assigned to the X-field. A second value can be entered in the Y-field and, if necessary, a third value in the Z-field. Finally, the desired function button is pressed.

The individual Radio-Button mean: Y(S) = Value of the store is assigned to the Y-field. X(S) = Value of the store is assigned to the X-field. Y(R) = Value of the RAM is assigned to the Y-field. X(R) & Y(S) = Values of the RAM and the store are assigned to the input fields X and Y. X(S) & Y(R) = Reversal, values of the store and of the RAM are assigned to the input fields X and Y.

To see the value of the RAM, press the button [calram]. The contents of the store are called up with the button [calsto]. If a radio button is activated, an entry in the field assigned to the radio button is not possible. However, the value from the working memory (RAM) can only be assigned once to the X- or Y-field via the Radio Button X (R) or Y (R), since the further calculation overwrites the working memory (RAM) with a new value. In this case, new values can also be assigned to the X- and Y-fields. With the radio button underneath the word "Result" the allocation of memory data to the input fields X and Y is deactivated. The assignment of values via the radio button X (S) and Y (S) can be done as often as required, as long as the store is not overwritten with a new value.

Button: enter By pressing the button [enter] a value written in the X field is transferred into the working memory (RAM) of the calculator. From there the value can be used by activating the radio-button X(R) which means that the value is assigned to the X-field. The second value is entered in the Y-field and, if necessary, a third value in the Z-field. Finally, the button with the desired function is pressed.

The following description is only for the stand-alone Mobile Phone versions: By pressing the button [x + y] without any numerical values in the X- and Y-fields, a blue link "Instructions" appears at the lower left edge of the calculator. After studying the instruction manual you can jump back to the calculator at any time using the arrow key of the Mobile Phone.

Button: store

The last value from the working memory (RAM) or from the result field can be copied into the permanent memory (ROM) with the button [store]. The value in the working memory (RAM) is not set to zero. The value in the permanent memory doesn’t get lost even in case the calculator is switch off.

Button: calram The value from the working memory is loaded into the result field. The value can be further used by activating a corresponding radio-button.

Button: calsto The value from the permanent memory is loaded into the result field. It will not overwrite the value in the working memory! The value can be further used by activating a corresponding radio-button.

Button: delram

The working memory is deleted and set to the value 0. The entries in the X-, Y- and Z-fields are deleted at the same time.

Button: delsto

The permanent memory is cleared and set to 0. The entries in the X-, Y- and Z-fields are deleted at the same time.

Button: del

The entire content of the selected input field is deleted. The contents of the other input fields, the working memory and permanent memory are not deleted.

Button: 10^ Base 10 for the input of an exponent. In front of the sign E must be set a number, behind the sign E the exponent,

e.g. 10-5 = 1E-5.

Button: & & is a placeholder in the Y-field between the value of the starting deposit and the rate / month in case of instalment savings. & is also a placeholder in the Y field between the total value of the object and the down payment in case of leasing calculations.

Button: J, M, W und D Abbreviations for time units: J = year, M = month, W = week and D = day.

J, M = conversion of the time unit from J years to M months, etc.